One of the main challenges for Carlos Tavares, as the newly appointed CEO of the FCA-PSA merger, is finding the right positioning for each of the fourteen car brands that are now under the same group. There is no other car group with such a number of brands in its portfolio, not even General Motors (8), Renault-Nissan (10) or Volkswagen Group (12) face such a difficult feat. What’s likely to happen to these brands and what role will they play?

The purpose of any merger is to reap the benefits of a larger market share and see potential costs savings. However, a big part of a merger’s success is determined by how the new company tackles both the strengths and weaknesses of the combined assets. It is important that the new siblings do not compete with one another to ensure the merger can expand the group’s presence in the market.

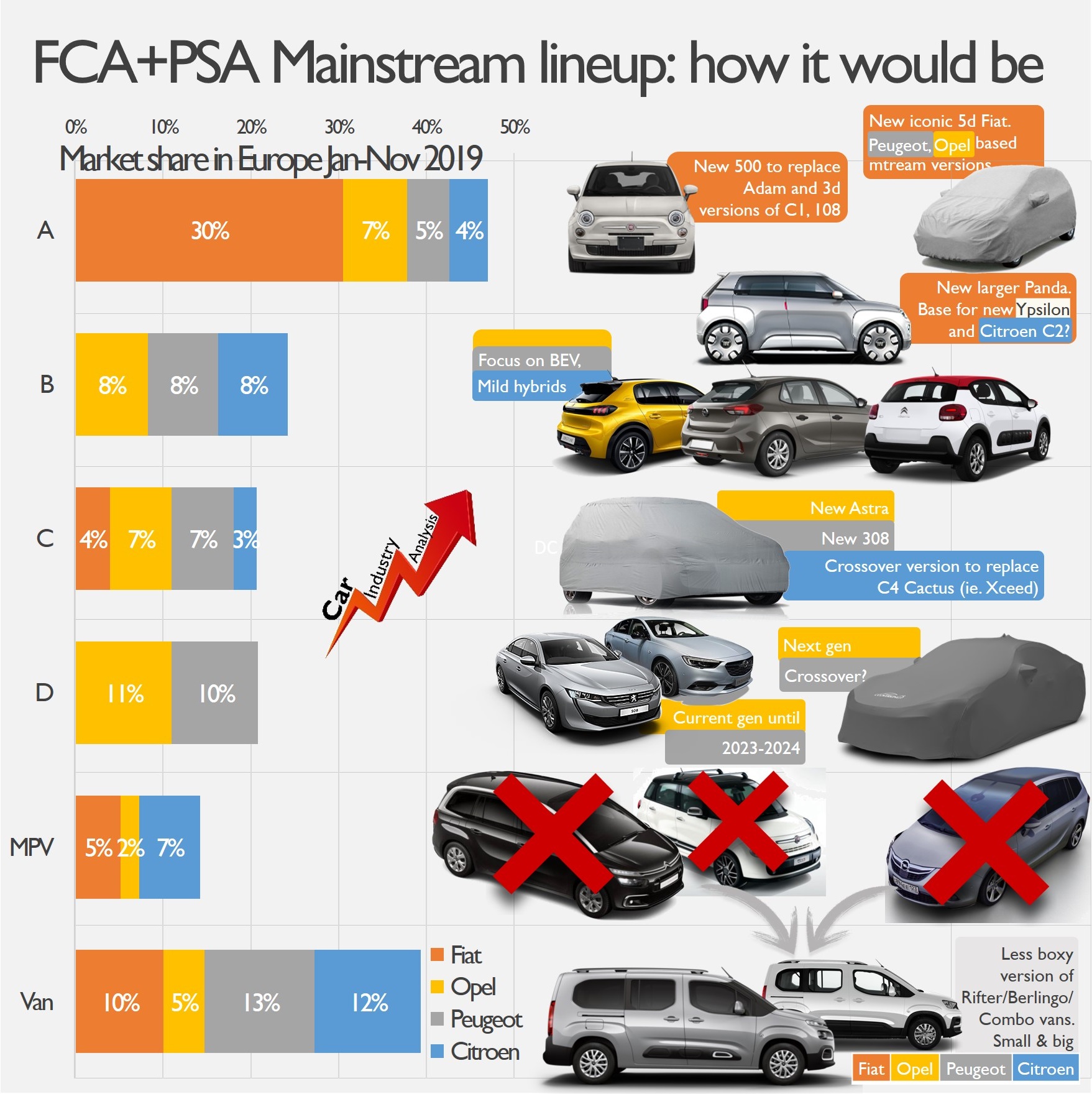

Fiat against Peugeot, Citroen and Opel?

The Fiat brand presents the biggest area of uncertainty for the new group. It currently faces a number of challenges, including an aging lineup, lack of key models and minimal presence outside of Italy and Brazil. In contrast, Jeep is an appealing counterpart, benefitting from a strong reputation among consumers worldwide.

Fiat’s global sales highlights the difficult situation the brand is facing. In 2009, when Chrysler Group was acquired by Fiat Group, brand sales accounted for 3.7% and 8% of global and European markets respectively. However, as of November this year, market share has fallen to 1.5% globally and 5% in Europe.

Alongside the need to renew their model lineup, Fiat must work to strategically position themselves in the market. The lack of brand identity means it is difficult to both describe and place Fiat within the automotive landscape. Over the last two decades, their product plan has lacked strategic vision, including an unusual combination of city-cars (Seicento, 500, Panda, Uno, Mobi), big wagons (Croma, Freemont), midsize pickups (Fullback) and sport cars (124 Spider, Coupe, Barchetta).

Carlos Tavares intends to reposition Fiat as the ‘small car’ brand of the new group. It is likely that the strategy will place Fiat in a new field, away from its siblings – Peugeot, Citroen and Opel. This is because it would be difficult to add a fourth mainstream player to the already crowded portfolio.

It is likely that the new strategy will place Fiat in a new field, away from its siblings – Peugeot, Citroen and Opel.

As a result, Fiat will be able to operate in a new segment and make use of its best values: charming, friendly, lovely and funny cars. Instead of adding more models in the B and C mainstream segments, that would most likely result in cannibalisation alongside its French and German cousins, Fiat will be able to focus on iconic models, including city-cars, subcompacts, small SUVs and small MPVs. It is important to consider that city-cars accounted for 42% of Fiat global passenger car sales in H1 2019, and more than half of its volume in Europe.

This repositioning would exclude the Punto and Tipo from the product plan for the coming years.

DS or Alfa Romeo

The other big question that emerges from this merger is how the premium strategy will take shape. The current state of affairs for the Alfa Romeo and DS is quite complex. For instance, despiteDS Auto recording a sales increase of 8.2% to 43,700 units in September 2019, it is facing serious issues with its line-up. Apart from its two SUVs, the remaining products posted double-digit sales decreases and two of them are due to leave the market shortly.

FCA is also facing a number of challenges, with predictions for Alfa Romeo 2019 sales dropping to less than 100,000 units – this being approximately 25%-28% less than in 2018. This negative trend seems to be in juxtaposition to their product offensive that began in 2016, featuring the Giulia and Stelvio. Nonetheless, the lack of new products since 2017 has damaged the expected growth seen in 2018.

It seems that the new group will aim to position the brands in differing markets. For example, DS is likely to boost its Chinese operations through new products that could eventually arrive in Europe, while Alfa Romeo will focus on North America and Europe, receiving a lifeline from the incoming Tonale C-SUV. Nevertheless, this does not mean that either brand is safe from failure. If the strategy does not work, DS does not have a healthy heritage to support it.

Jeep to share its SUV DNA with Peugeot and Opel

Tavares is aware that Jeep is the crown jewel of FCA, however, despite new vehicles expected to hit South America and European markets in 2020, the brand needs more products. To achieve this, the best approach would be to share the costs with other mainstream brands – and the best candidates are Peugeot and Opel.

As Opel hopes to expand its presence outside of Europe, presenting itself as the German brand of the group, they could start developing SUVs in collaboration with Jeep. With Jeep positioned as the American off-road lifestyle-oriented brand, its SUVs could instead wear a mainstream European style under Peugeot and Opel brands. On top of this, we must remember that SUVs accounted for 40% of PSA+FCA’s passenger cars global sales in H1 2019, and Jeep represented 49% of its SUV volume during the same period.

Lancia and Vauxhall will survive

It is unlikely that the newly merged company will discontinue Lancia in Italy and Vauxhall in the UK, as they are not the only unique-country car brands in the world. For example, Holden is only available in Australia and New Zealand, Jetta operates purely in China, and Samsung exists solely in South Korea. In the case of Lancia, the brand could benefit from the new Fiat city-cars/SUVs replacing the current Ypsilon, one of the top-selling cars in Italy.

Source: JATO Dynamics, Goodcarbadcar.net, Bestsellingcarsblog.com, ACEA, FGW Database

I really expetc that peugeout and citroen increases their sellings in Brazil!

LikeLike

Happy end, at last 👌

LikeLike

So I like to read your analyzes but I am wondering when you do them how do you get your info or it’s just a suggestions. I agree with most of the stuff but some just look like it’s not exactly clear. Example: It says new quattroporte will be an anti 8 series . From what I know one is sedan and one is coupe(totally different cars and I don’t see how they can compete against each other). You are doing a great job overall and the articles are interested. Will be nice if there were more posts

LikeLike

Thanks Justin. I meant a rival to the 8 Series Grand Coupe

LikeLike

If they only could grew their offerings as much as the germans then will be possible otherwise if they go against 8 series grand coupe they wont have one to fight the 7 series so it’s tit for tat even though will make sense any Maserati to be really sports focused than anything else. Maybe Ghibli should go against it and let Alfa fight 5 series and lower, but again it’s all wishful thinking kind of far from the reality at least for the time being . It seems like will be really hard task to revive both of those brands and make them profitable in a long run

LikeLike

FIAT become the brand I have been asking for since FCA tie up.

Competitor for MINI.

They have the history and the style to use the 500 design and make a range of cars off the PSA platforms

500 3dr hatch and EV (108,C1)

600 5 Dr hatch, cabrio, SUV, wagon, replacement for Punto, off 208 platform.

Do not sell on US, but rest of the world.

LikeLike