Colombia is going to be the first market to be quickly analyzed from the point of view of its overall composition (by brands and segments), and the position of Fiat-Chrysler. Since it is quite difficult to do a close analysis (as I would like to) of every single market where the group sold cars last year, I will try to be very clear and concise with the following posts. Colombian car market is having a great momentum thanks to political and economic stability. Even if the passenger car market is down 5% year-on-year, the market had its second best year with more than 285.000 units (LCV market, which includes trucks only, is up a massive 24% to 31.000 units). Hence, Colombia is Latinamerica’s 5th largest car market, but it is the third most populated country after Brazil and Mexico. This means the new car/1000 inhabitants index is very low compared to its neighbours, and there is still a big potential for growth.

Colombia is going to be the first market to be quickly analyzed from the point of view of its overall composition (by brands and segments), and the position of Fiat-Chrysler. Since it is quite difficult to do a close analysis (as I would like to) of every single market where the group sold cars last year, I will try to be very clear and concise with the following posts. Colombian car market is having a great momentum thanks to political and economic stability. Even if the passenger car market is down 5% year-on-year, the market had its second best year with more than 285.000 units (LCV market, which includes trucks only, is up a massive 24% to 31.000 units). Hence, Colombia is Latinamerica’s 5th largest car market, but it is the third most populated country after Brazil and Mexico. This means the new car/1000 inhabitants index is very low compared to its neighbours, and there is still a big potential for growth.

Source: Revista Motor

The market is dominated by 3 major players: GM, Renault and Hyundai-Kia. Chevrolet, which has the largest number of dealerships and an assembly plant in Bogota, controls 30% of the market. It is followed by Hyundai-Kia, which has gained several positions in the last years and now it has 19% of market share. Renault comes third with 15% share, even if it has an assembly plant in Medellin and the Koreans import all their cars (Colombia and Korea have just signed a FTA, so Korean cars will become even cheaper in the coming months). Chinese brands are also gaining market share thanks to entry-level mini cars and the taxis. The composition of the market by segment shows that Colombians prefer B-Segment cars (32%), SUVs (22%), and city cars (18%). Normally, most of the car makers have several offer in B-Segment and they mix the old generations with the new ones: Renault offers the old Clio (second generation), the Sandero and the Logan. Chevrolet has the Aveo, Cobalt, and Sonic. The market reflects the big differences between social classes in Colombia: ‘D’, ‘E’ and ‘F’ segments count for only 1,38% of total sales.

Fiat brand doesn’t include Taxi’s registrations. Source: Revista Motor, Colitalia Autos

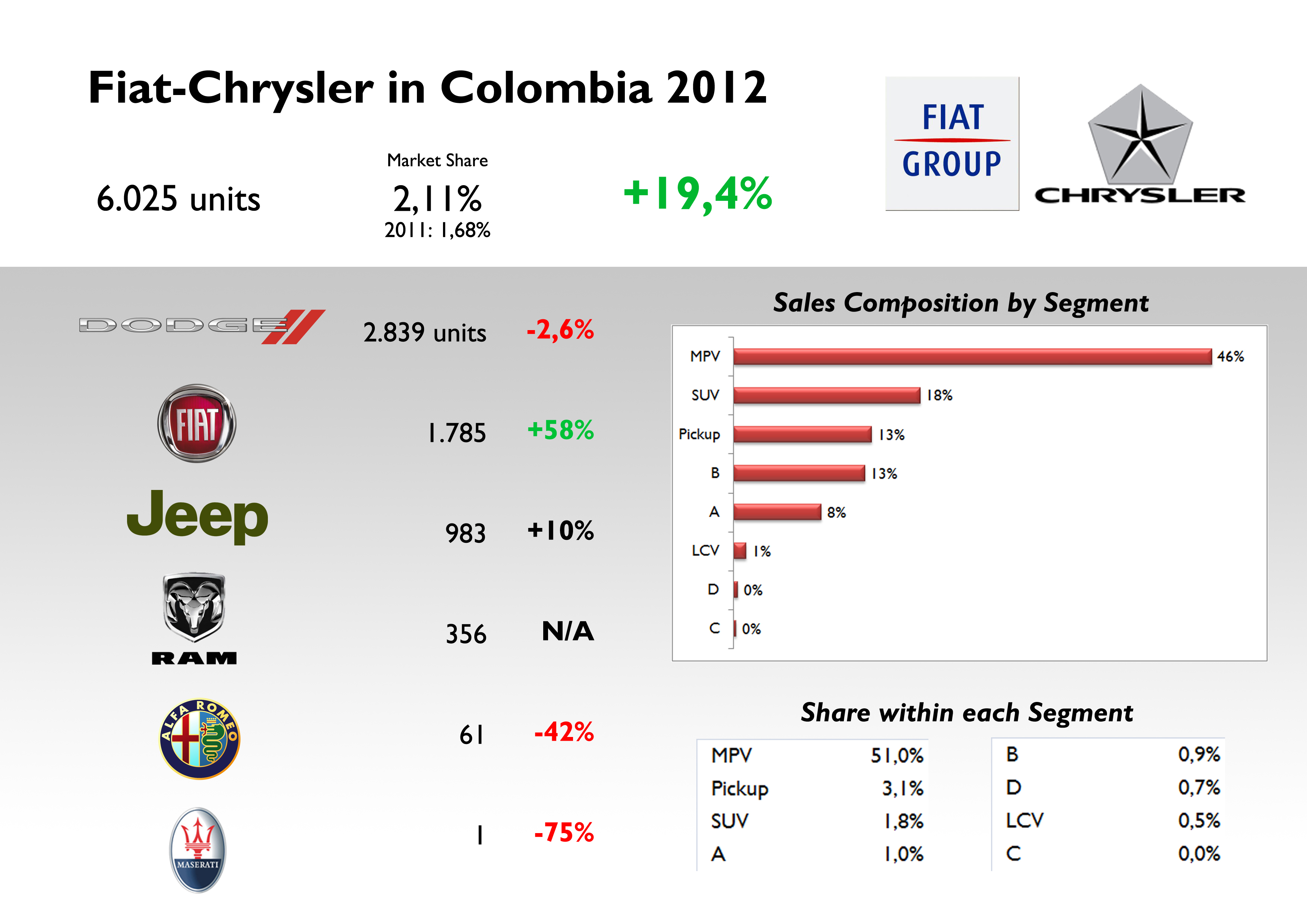

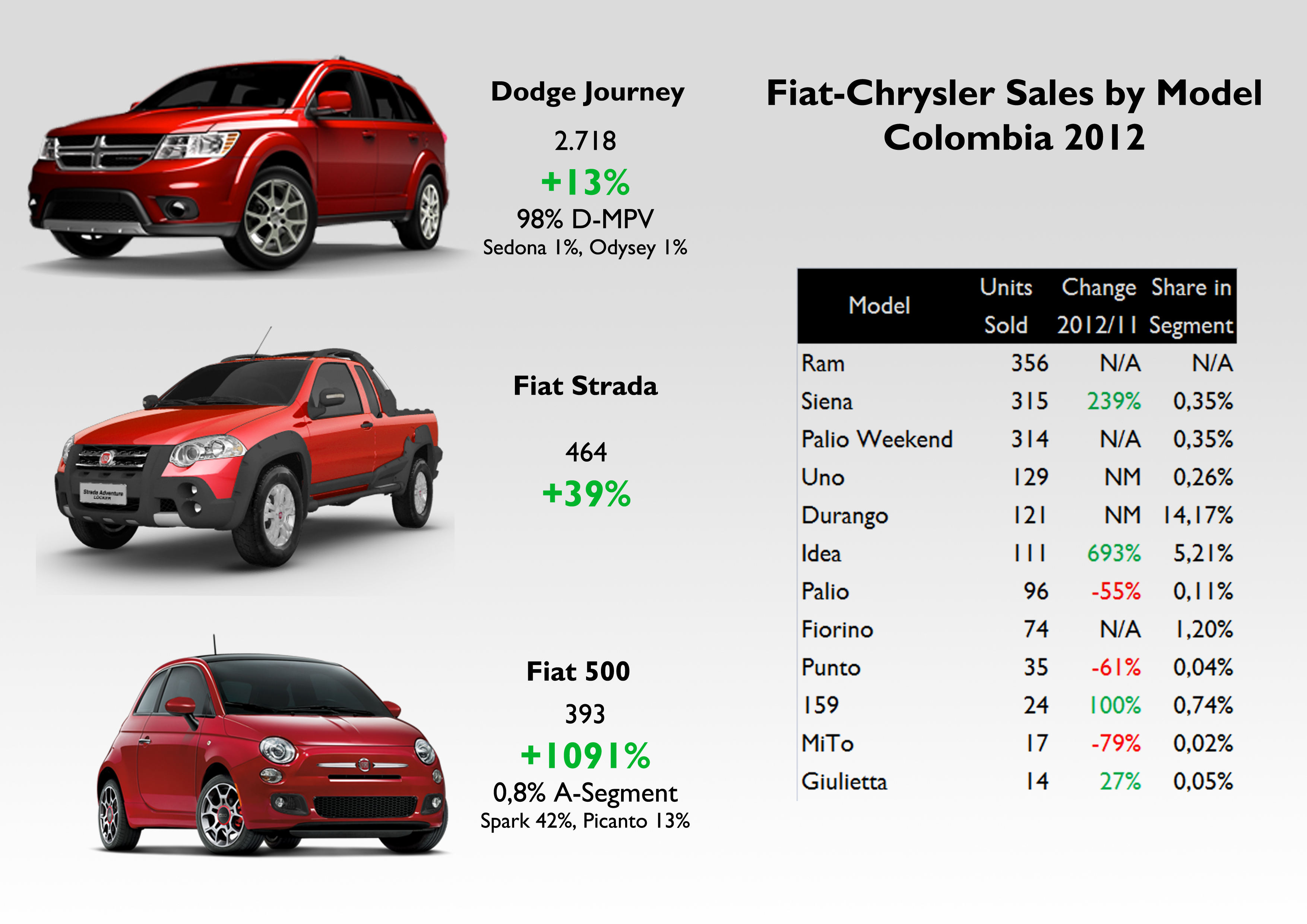

Fiat-Chrysler improved but needs to do more. In 2012 it sold more than 6.000 units, up 19%. Chrysler division counts for 69% of sales, as Dodge is quite popular thanks to the Journey. However, its sales fell 3%, while Fiat brand jumped a massive 58%, and Jeep grew 10%. The group controls 2% of the market, which is considerably low compared to Brazilian, Argentinian, or Venezuelan market shares. The good job Colitalia Autos (official importer) has done with Fiat and Alfa Romeo, has allowed both brands to gain some awareness, and in the case of Fiat, a better image, after years of bad service. Thanks to the FTA between Mexico and Colombia, the group is doing very good with the Mexican Journey and 500, both with interesting numbers. Other important products are the pickups Strada (from Brazil), and the Ram Pickup (USA). Things will get more difficult for the group as competition will get harder with the arrival of tax-free Korean cars. Additionally, Fiat is running out of new products (most of them come from Brazil), while Alfa Romeo doesn’t know what else to do to impress the market (lack of products). Nevertheless, Jeep will benefit from the arrival of the new Cherokee (available in the Q4), and less import taxes (consequence of the FTA between Colombia and USA). Another opportunity will come from Europe, as Colombia has just signed a FTA with the EU, and European cars will be able to enter the Colombian market paying less taxes. This could be the chance for the arrival of the Panda with better prices. Fiat and Alfa Romeo plan to sell around 3.000 units in 2013, while Jeep and Dodge may increase their sales to 5.000 units.

No data for Jeep. Source: Revista Motor, Colitalia Autos

Many thanks to my friend Manuela Todeschini from Colitalia Autos Colombia